USDA and VA loans have the least restrictions on home mortgage gifts. Anyone you have a relationship with can offer a down payment gift, however the one caveat is that they can't be an interested party. An interested party is somebody associated with your home purchase transaction, for example, your realty agent.

It's called a home loan gift for a factor the gift giver is providing funds to a house buyer with no expectation of being repaid. If the purchaser is planning to pay back the funds, that cash was loaned not gifted, and after that the loan provider is required to element that into the debt-to-income ratio.

Keeping details about your deposit sources could put your loan credentials at danger, and even more notably, it's thought about home loan scams, which is unlawful. The bottom line: Be sincere with your lending institution about home loan presents and where you're receiving your down payment funds. Your lender will require paperwork proving the down payment cash has actually been received by the home purchaser.

Experienced funds are those that have actually been in the house purchaser's savings account for an amount of time. Generally, funds that have remained in your checking account for at least 2 months won't be questioned by your lending institution, due to the fact that it's seasoned money. Before you can use gift funds for your deposit and/or closing expenses, you need to send a gift letter to your loan provider.

How What Are The Interest Rates On Reverse Mortgages can Save You Time, Stress, and Money.

Your gift letter should include: The dollar quantity of the gift The date the funds were transferred The donor's signed declaration that no repayment is expected The donor's name, address, and contact number The donor's relationship to the debtor The donor's relationship to the purchaser The address of the property being purchased Talk to your lender about what details they need in the present letter.

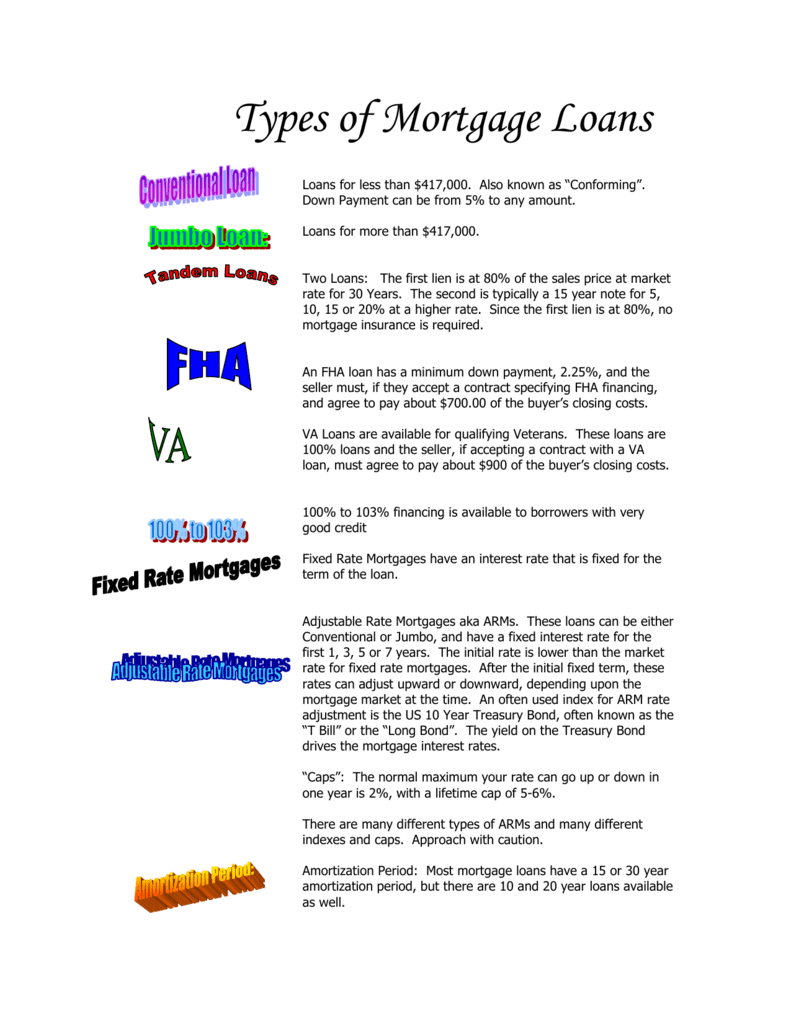

Different loan programs have varying limitations on the quantity of money a buyer can get as a present and other considerations. Here's a breakdown of some of the most common loans: Your whole down payment on a one-unit primary house can come from a present. For 2- to four-unit main properties, a 5% minimum deposit from your own funds is needed from Fannie Mae and a 3% down payment from your own funds is needed by Freddie Mac.

If it's less than 20%, then 5% of the down payment is required to come from your own funds. All these situations need proper present documentation. The whole minimum 3 - what the interest rate on mortgages today. 5% deposit can be talented as long as the gift is appropriately documented. VA loans do not need down payments, but they permit borrowers to utilize effectively recorded present funds towards a deposit if they pick to.

The person receiving the present will not be accountable for any tax liability, however the gift giver may be accountable if the amount exceeds the gift tax exclusion limitation. As of 2020, a person can gift approximately $15,000 without a tax penalty. That means a couple filing collectively can quit to $30,000 and won't be required to report it to the IRS.

How Who Took Over Taylor Bean And Whitaker Mortgages can Save You Time, Stress, and Money.

Home loan gift donors must inspect with their tax consultant or accountant to more accurately identify how a gift that exceeds the exemption limit will affect their financial resources. Be upfront with your home mortgage lender if you're getting a down payment present. Tell your lending institution you're receiving a gift if there's an expectation to pay back the funds.

Fail to divulge a gift you have actually currently gotten to your loan provider. Make certain the gift is coming from an allowed relationship depending on your loan. Forget federal tax gift exemption limitations. Gift funds are a lifeline if you are prepared to acquire a house however don't have adequate money.

Fortunately is that there are other possibilities readily available for when you're facing low deposit funds. While it may not be your first choice, one option is to consider extending your timeline for buying to offer you more time to conserve money. Or, you can try to find other methods to increase your capital, such as handling a sideline or beginning a side hustle.

You might be able to receive a grant that provides money to property buyers for a deposit and in some cases closing expenses. Some loan programs, like VA and USDA, require no down payment for certifying borrowers. FHA loans and standard loans are excellent alternatives if you do not meet eligibility requirements for VA or USDA.

Our Who Took Over Washington Mutual Mortgages Diaries

5% for FHA and 3% for standard. Give us a call to see if you're qualified for a low deposit loan.

The short response is possibly. The longer answer is that it depends upon the type of loan and the lender. The present needs to be from your domestic partner, future husband, or relative if you're going with a standard loan. This can consist of current and future in-laws, nieces, nephews and children as well as parents, grandparents, aunts, uncles and brother or sisters.

Aside from relatives, this type of home loan may permit loans from friends who show they have a clear interest in your wellness. A charitable organization, labor union and even your company might have the ability to present you a deposit. If you can get approved for a USDA or VA loan, these are even looser with their guidelines.

Examples of forbidden donors include your genuine estate agent, a home builder or developer, and the seller. Once again, these are general guidelines for these types of loans. For insight into your particular circumstance, speak to a home loan specialist.

The Ultimate Guide To What Banks Use Experian For Mortgages

Conserving a down payment is among the most importantand typically most challengingaspects of purchasing a home. The larger your deposit, the less you need to fund, which can cause lower rates of interest and regular monthly payments over the life of your loan. Moreover, a large deposit can help you avoid pricey personal home loan insurance coverage.

In a 2017 Zillow study, nearly 70% of occupants stated conserving a down payment was the most significant hurdle to buying a home. If you're prepared to end up being a house owner, asking your family for help with your down payment may have crossed your mind. While down-payment funds can be gifted in between household members, you should follow a list of guidelines to document the present, including a down payment gift letter.

If you have a credit report of 580 or above, you might be qualified to get an FHA loan with a 3. 5% deposit. If your credit rating falls listed below 580, you will require to put a minimum of 10% down. If your credit rating falls between 580 and 619, then 3. The gift, depending on its amount, might likewise substantially decrease your month-to-month home mortgage payments in the coming years. If you have actually conducted comprehensive research of the rules and guidelines, think about having a kind associate or family member help you with a money infusion. Receiving a cash present for the purpose of covering deposit on a home or home mortgage payments can be a practical.

Simply make you have a comprehensive gift letter. A terrific credit score brings fantastic results, especially with homeownership. If you preserve a high credit history, you might be eligible for better home mortgage rates, which result in lower regular monthly home loan payments. Purchasing a home should not indicate compromising your other financial goals! If you're unsure whether homeownership is in the cards for you at the moment, consulting with a financial consultant could be your finest move.

What Do Underwriters Do For Mortgages - Questions

By addressing a couple of concerns about your financial resources, the program will pick approximately 3 fiduciariesout of a pool of countless advisorswho directly match your requirements. This cuts https://storeboard.com/blogs/general/9-easy-facts-about-what-does-hud-have-to-with-reverse-mortgages-explained/4543647 your heavy lifting in halffor free. Picture credits: iStock. com/urfinguss, iStock. com/Steve Debenport, iStock. com/elise _ kurenbina.

Say you have actually just married and received a piece of money to put towards your deposit. Although you might be excited to get that money in the bank, you do not want these deposits to trigger problems when you're attempting to get approved for a home loan. Let's review some extra details on how present money effects home mortgage underwriting.

As long as you have documentation for the previous 60 days, your home loan business can take it from there. So, within that 60-day duration, which deposits do you need to stress over getting a gift letter for? Get your wedding event veil and delve into this theoretical situation with us for a moment.

Aunt Sue offered you a $75 check, but Grandmother Betty provided you $10,000 for getting married (you have actually constantly presumed you were the preferred grandkid). Will you require present letters for both deposits? In general, your underwriter will need to validate the source of any big deposit. What's the requirements for a "big deposit"? For standard, VA and jumbo loans, it's any single deposit that surpasses 50% of the overall monthly certifying earnings.

Not known Facts About What Type Of Mortgages Are There

In this example, let's say you're doing a traditional loan. If you make $4,000 a month, any deposit over $2,000 would most likely be questioned by your underwriter. Therefore, the underwriter will most likely wish to confirm that Grandma Betty's $10,000 present is a gift, not a loan, so you'll require to ask her for a present letter.

Obviously, this is partly up to the underwriter's discretion. If there are any deposits that seem to be uncommon, your underwriter might question them regardless of your income. If you normally had $2,000 in your bank account and you suddenly have a deposit for an additional $8,000, they would wish to confirm that no matter the purchase price/appraised worth or certifying income.

Although your Aunt Sue's little present might not be doubtful in and of itself, if the underwriter finds that it's out of the normal, they might require present documents. You can certainly write a present letter from scratch, and it can be as official or casual as you 'd like. The only caveat is that it must consist of the required details. When writing your gift letter, make sure you consist of: Donor name, address, and phone number (You will require this for each donor if you have more than one) Nature of relationship The specific amount of the gift funds Plainly describe that repayment of funds is not required Payment method for the funds Address of the home you will purchase You can use this present letter template for your circumstance.

You might be questioning why you require to state that a gift is a present. It's a good question. As you go through the home mortgage procedure, your loan provider will assess your loan throughout numerous actions. One of the most crucial of these actions is the underwriter evaluation. Underwriters give final approval on your loan.

How Which Of The Following Statements Is True Regarding Home Mortgages? can Save You Time, Stress, and Money.

Due to the fact that they scrutinize your finances, big deposits without explanation are a red flag. Offering a gift letter is essential as it describes the source of your funds. The present letter is not all either. In addition to the present letter, your underwriter will need to verify your funds. Verification consists of bank declarations and might require proof from your donor to reveal the money leaving their account.

In this case, that would be a gift letter. There are a number of other letters of explanation you might require, such as explaining a credit event. With that stated, originators are surprisingly flexible. We desire to get you authorized!.?. !! But we still need to follow the requirements for each loan program.

In general, FHA loans include fewer regulations when it concerns gift letters. To start, all funds for your deal can come from a gift. FHA loans are more lenient because they are federal government programs created to guarantee homeownership. FHA loans also include low credit report and down payment requirements however typically featured mortgage insurance.

Like FHA loans, standard loans permit you to money your deal utilizing gifts entirely. Nevertheless, if you are acquiring a secondary house, you will require to provide at least 5% of the funds to prevent mortgage insurance. You will likewise find that standard loans featured more restrictions when it concerns the funding source.

What Fico Scores Are Used For Mortgages Fundamentals Explained

Nevertheless, Fannie and Freddie do not require the source of the donor's funds. USDA programs are limited to rural areas however offer zero down and also enable you to use gifts. The same sources as FHA loans are allowed with the caution that friends have actually a recorded relationship. Present funds for USDA loans can be utilized towards closing expenses.

VA programs work similarly to the other loan programs discussed. With VA loans, the only limitation is that gifts can not come from somebody with a beneficial interest. Va loans themselves provide some fantastic advantages for veterans. Like any other, with VA loans, a loan provider will likewise wish to verify whether gift funds exist by asking for evidence of a certificate of deposit or bank statement.

Because presents towards your home mortgage are typically big quantities, it may be required to report your gift to the Internal Revenue Service. Although the donor is typically the one responsible for paying taxes on the gift, there are some unusual situations in which the recipient can consent to pay it. It's not most likely you will need to involve the IRS, nevertheless.

You might not need to report your present if it is less than $15,000 and you are applying for among the following years: 2018, 2019, 2020, 2021. When you have your present letter prepared, send it to your underwriter or home loan specialist unless you have actually been directed otherwise. The letter of gift will be included to your file and make sure underwriters have no reason to hold up your closing! You are now one step closer to getting into your dream house! Gift letter guidelines have not changed much throughout the years.

The Best Strategy To Use For Why Reverse Mortgages Are A Bad Idea

It provides underwriters the evidence they need to be confident in the financial investment and make your imagine homeownership a truth. Here at On Q Financial, our company believe the dream is inclusive and will deal with you every action of the procedure to assist guarantee your dream is understood! * Info goes through alter without notice.

Some constraints may use. This material is supplied for information and academic purposes only. Constantly speak with a professional advisor prior to making monetary decisions. OnQ1124200681Y00000AzsRl Before opening On Q Financial in 2005, John Bergman came from and moneyed 450 systems a year as a loan officer. He founded the business with just $1M of individual life savingscommitted to his vision for building the very best independent mortgage company in the industry.

By Brandon Cornett 2019, all rights scheduled Duplication free timeshare vacation packages prohibited Numerous home loan programs available today allow borrowers to utilize gift cash from an approved donor, such as a member of the family of friend. But they likewise require the borrower to acquire a "gift letter" from the person( s) providing the funds.

It likewise discusses the basic rules and requirements for these letters, according to the various loan program guidelines. For lots of home buyers, the down payment represents the biggest financial difficulty they most overcome when purchasing a house. Depending upon the kind of mortgage you are using, the minimum required down payment may vary from 3% to 20% of the purchase rate.

Getting The What Do Mortgages Lenders Look At To Work

The good news is that customers do not necessarily have to pay the entire thing out of timeshare their own pockets. In most cases, house buyers can use gift money to cover the down payment and/or closing expenses related to a mortgage loan. Conventional, FHA and VA mortgage permit borrowers to utilize gift cash from a third celebration to cover some-- and even all-- of their down payment expenditure.

The one thing they have in typical is that all of the home mortgage programs require the customer to get a present letter. (See the sample design template listed below.) Home mortgage down payment present letters do not have to be intricate or prolonged. They simply have to strike a few essential points. While the particular requirements can differ depending on loan program, there are some common "components." required throughout the board.

It must not be written by the debtor/ house purchaser. That's an essential point. The main function of the letter is for the donor to inform the loan provider that they are giving the money freely and do not expect any sort of repayment. So it must be composed and signed by the person who is gifting funds to the borrower.

The amount of money they are providing you (exact dollar amount). The date of the present/ contribution. A declaration validating that they do not anticipate repayment. Address of the home being acquired (in some cases). The donor's signature. Item # 4 above is the most essential item on the list.